Case Study

A Credit Union’s Data-Driven Business Transformation

Background

In today’s highly competitive and regulated Credit Union sector, companies are constantly seeking innovative ways to optimize operations, ensure compliance, and enhance member satisfaction. This case study explores how a leading American Credit Union utilized Call Journey CI for conversation analysis of member conversations across voice and non voice channels to identify and capitalize on 6 different categories for business improvement, resulting in a staggering $7.5 million in potential savings – just over $4.6m of that in tangible and directly measurable cost/business benefits.

The Challenge

Market Challenge

The Credit Union faced the challenge of identifying untapped opportunities for improvement across multiple lines of business, as well as capturing the Voice of the Member (VoM) in a timely manner. Traditional approaches to data-driven business transformation were not yielding the desired results, and a survey-based approach to VoM measurement meant that it was difficult to close feedback loops in a satisfactory timeframe. The Credit Union sought a fresh solution to uncover potential areas for improvement.

Organization Specific Challenge

Leveraging better and smarter data for better decisions and business impact

With the credit union managing over 60,000 phone conversations per day with its members and between 3,000 to 5,000 non-voice interactions spread across 6 different contact centers in different regions, the credit union was finding it hugely challenging to homogenize, augment, and understand the volume of disparate interactions they were having.

Traditional approaches to members, operations, and employee (agent) intelligence were frustrating them in that they felt like the data wasn’t accurate enough, supplied them enough context, and certainly wasn’t proving them, the overall level of intelligence that they desperately needed.

The Member Experience VPs were frustrated at the lack of insightful data and the absence of a qualitative and quantitative view of where the actual challenges were.

We knew we were making bad decisions with bad data before we were introduced to Call Journey. Our initial assesment showed us that a staggering 63% of agent summaries / disposition codes were incorrect, and as a bank we were making some pretty bad decisions and bets based on this data / intelligence

Chief Member Experience Officer

The Contact Center VP and Operators were frustrated similarly in that the key initiatives that they were driving lacked effective intelligence, hampering the success of those initiatives.

We’ve been on a big drive to self service and automation, but the initiatives that we had in play weren’t shifting the dial as we’d hoped – we figured there must be something wrong and we soon found out it was the data that we were getting to help drive the areas of focus

VP for Contact Centers

There were a number of operational challenges for the credit union, but they decided to focus on four areas of statistical performance concern:

- Cost per Contact was unfavorable by 17% ( -17% unfav). The credit union derived cost per contact by dividing the total operational costs, including agent salaries, infrastructure, and overheads, by the total number of calls handled within a specific period.

- Their digitization/automation/self-service program was lagging by 33% to their cost-out target and other measures below were also lagging (-33% to cost-out target). The credit union set itself internal goals to shift call volumes from voice to self-service and part of that program included finding interactions that could be digitized, automated, or provided to their members as FAQ. The initiative also had cost-out benefit goals attached.

- Speed to resolution was unfavorable 15% ( -15% unfav). Speed to resolution was a measure the credit union raised as quite important, as the goal was to reduce repeat callers and create better coaching activities to improve agent knowledge based on the types of calls that were causing lengthy contact (higher AHT), repeat contact, and dissatisfied members.

Agent productivity was lagging by 38% ( -38% unfav). The credit union like most contact centers, had an agent productivity measure. In this case, the credit union looked at AHT, speed to answer, logged in and available and total FTE count aligned to workforce planning. In short, if their call volume or call duration went over the forecast/budgeted goal, they had to either: reduce the call handling time or hire more agents. This was a key measure because even a small error in capacity planning meant a significant cost overrun in agent / FTE costs.

There were some pretty hairy challenges we were trying to stare down as a credit union, and looking at result pre adopting Call Journey Ci, we were clearly flying blind because we were behind in four of key metrics

VP of Operations

The Selection

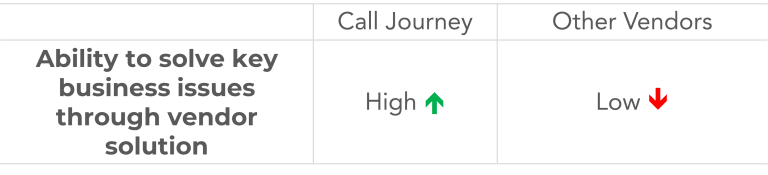

What was really confusing to us a credit union member experience leadership team, was that so many suppliers in the market were telling us that their technology would help us solve some of our key member experience problems. Many vendors told us they did things like topic analysis/keyword spotting to uncover important data, others told us that they uncover member needs at scale.

Additionally, as a credit union, our internal resources were limited and stretched and whilst a key decision point for us was to find a vendor solution that provided the level and sophistication of data and intelligence required, we were looking for a solution that took us as close to action as possible – i.e we were looking for the solution to tell us the story behind the data, not just present us the data for us to wrangle.

Lastly, we were looking for speed to value and high ROI. We didn’t want to engage a vendor solution that then saw us having to do the heavy lifting around our key uses cases as once again, we didn’t have capacity.

When we had the chance to do a discovery session with Call Journey Ci, see the platform in action and understand its delivery we were blown away. The key points for us in deciding to partner with Call Journey Ci were:

- Far better layers, detail and color in their data – context-aware data, multi-layered and to the level of granularity we would expect most members would need

- Deep layered intelligence vs basic topic analysis and word spotting – (again we didn’t want to make bad decisions with bad data)

- Business impact aligned insights – being able to straight away see and visualize business impact

- Out of the box key use cases with significant relevancy (straight away we could get to exactly why people were ACTUALLY calling, why they were dissatisfied, why our AHT was where it was and why we keep getting repeat callers for example

- Data Storytelling – Unlike basic analytics tools we were exposed to in the market, we saw that Call Journey Ci transformed complex datapoints into a compelling story, revealing root causes and actionable recommendations for us to drive real member impact with limited resources to assess the same data

- Their future state roadmap of solutions didn’t cost us anymore – we will utilize Call Journey’s Member Effort measurement module when it’s released alongside their automation/digitization assessment module.

Vendor Comparison

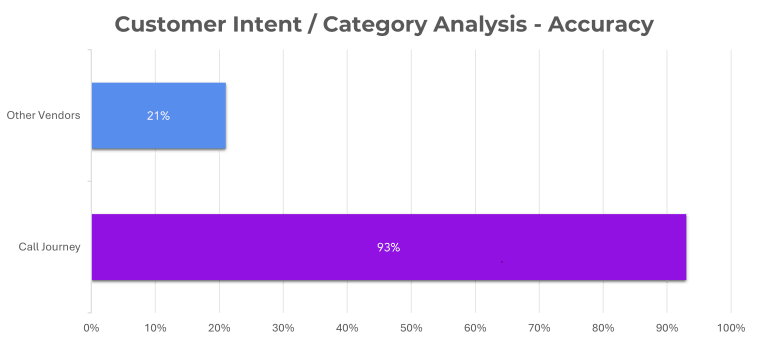

Call Journey unlike all other vendors utilized far more details relevant and context aware data mining techniques to surface things like root cause of member contact, root cause of dissatisfaction, and cause of high AHT and low FCR. All other vendors fundamentally were utilizing basic word-spotting and topic analysis which statistically showed to be surfacing inaccurate and misleading data and insights.

Call Journey Ci has extensive well-researched and constructed modules, reports, and insights based on common but key use cases, which meant we were able to hit the ground running with accurate and effective data and intelligence from the get-go.

Call Journey Ci seems to philosophically employ the approach of almost “business intelligence in a box” whereby we didn’t need to lean into our internal data science or BA capabilities because CJ had already done the heavy lifting for us thru effective and efficient data storytelling.

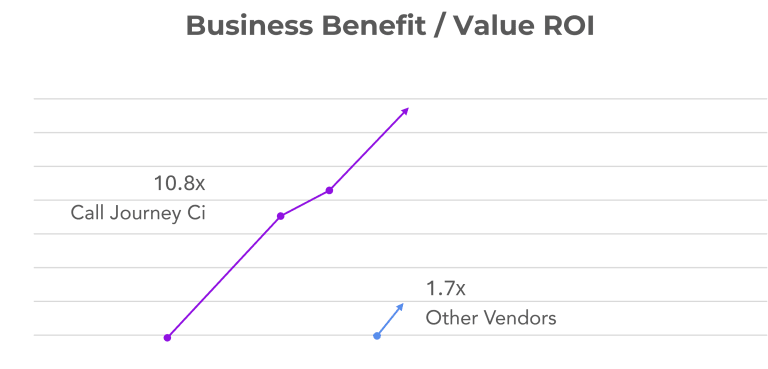

When we assessed potential ROI from the solutions available in the market, the combination of lack of accuracy and lack of relevant use cases (many vendors were still heavily agent AQM or coaching focus) showed a significant difference in business benefit, particularly because we could solve for high cost, high-impact business challenges vs. low-impact and piecemeal agent insights.

The Solution

How The Credit Union Uses Call Journey Ci

The credit union decided to explore conversation intelligence as a means of extracting valuable, actionable insights from member interactions. Leveraging advanced natural language processing technologies, advanced machine learning, and data science principals and models with Call Journey CI, the credit union embarked on an “always on” program to continually achieve effective data and intelligence from a comprehensive analysis of member conversations across various lines of business and contact types

Key elements/modules of the platform utilized were as follows:

- Dissatisfaction Analysis: Data science and AI/ML-driven analysis of what was truly driving dissatisfaction. Layers 4 and 5 of interaction assessments applied including the use of GenAi as a component of the solution to understand, categorize, and report on dissatisfaction. Elements include context and relativity and are achieved through qualitative and quantitative assessment.

- Root Cause Contact Analysis: Data science and AI/ML-driven analysis of what was truly driving dissatisfaction. Layers 4 and 5 of interaction assessments applied including the use of GenAi as a component of the solution to understand, categorize, and report on the key reason/s for customer contact. This is not a basic level of topic analysis common in the market to levels 1 and 2 at best, this is a comprehensive, levels 4 and 5 data-driven, precise assessment using sophisticated data science algorithms and models. Elements include context and relativity and are achieved both through qualitative and quantitative assessments processed on-premise with Call Journey CI’s PII/PCI capabilities, ensuring that customers’ identities are protected throughout the analysis process.

What was really confusing to us a credit union member experience leadership team, was that so many suppliers in the market were telling us that their technology would help us understand why our member were actually calling – nirvana for us as you could imagine! However, it wasn’t until we really dug into the different vendor solutions, that we saw a massive disparity of what we were actually getting in way of output and intelligence. Call Journey’s detail, levels of data mining, sophisticated modelling and multiple layers of accurate categorization, really stood out from the market. In the end, I’m relieved we decided to work with Call Journey’s platform, as the tests and proof of concepts we did with the other suppliers, was serving up poor data and incorrect interaction assessments.

Head of Member Service

3. Agent performance/productivity analysis: Data science and AI/ML-driven analysis of what was truly the key elements of agent performance and productivity. The models deployed were built with the contribution of a cross-section of our customer base.

Detailed and in-depth analysis was applied to four categories:

- Agent Conduct

- Agent Communication

- Agent compliance

- Agent empathy and integrations

4. Automation/Self-Service opportunity analysis (Was in Beta): Data science and AI/ML-driven analysis of what areas of interactions should be automated or digitizedakes into consideration numerous interaction insights and customer interaction elements and also applies contextual analysis alongside qualitative and quantitative assessments.

We’d struggled to really shift the needle in a meaningful way in our automations and self service/digitization efforts. Call Volumes weren’t decreasing anywhere near where we expected and the members experience with our digital and self service assets was actually pushing volume back into our contact center channels. Call journey’s platform, using Ai and it’s models, actually showed us were the focus should be based on the source we should have been mining properly in the first place – the lived experience of our members from the member mouth (and fingers!)

Member Experience Manager

5. Executive Summary and Recommendations (Advanced pilot): Data science and Ai/ML driven analysis of the dissatisfaction module and its insights, employing GenAi and model driven assesment of large data packages to drive insights and recommendations.

Initially, the bank reviewed the insights and recommendations every week to look for trends and issues.

- 5-6 weeks in, they shifted to a review every 2 weeks.

- 8 weeks after introducing the pilot module, they began to track performance changes based on new initiatives to address the problems uncovered

- 90 days into the pilot they began to see a correlation and shift in performance from the insights, recommendations, and actions taken.

Understanding the member journey is a huge challenge for anyone, and in the credit union with multiple products, platforms and systems, tracking and understanding the member journey, and most importantly the member effort in engaging with us, is a massive priority. Previous to Call journey Ci we’d relied on surveys and systems intelligence to give as member effort guidance, but again, this approach ignored the most important element of our member interaction – the member themselves. Being able to track and understand EXACTLY where the member friction points are in interacting with us, and where member effort is high, will be a game changer for us. Tapping into the actual lived experience of every member across every interaction and being able to score, assess and measure that is the game changer we were looking for!

Member Experience Manager

The Results

The conversation analysis yielded a total of well over 100 distinct opportunities for business improvement within the Credit Union, which they subsequently grouped into 4 different categories and focus areas. . They included process and service optimization, agent training, resource allocation, and technology enhancements. The potential savings/business benefit associated with these opportunities were estimated at $7.5 million in potential savings – just over $4.6m of that in tangible and directly measurable cost/business benefits.

Key Findings

Service Efficiency Improvements: Mined lived experience member intelligence highlighted areas where service delivery could be enhanced. Implementing changes in these areas have a defined result in improved efficiency and reduced operational costs.

Cost out : There were many new process, productivity and efficiency intelligence area found which had a large impact on reducing cost to serve whilst improving member engagement and experience. Further savings were identified in automation and process optimization.

Agent Training Opportunities: The Credit Union identified unique and specific areas of agent training that would help them meet their regulated member service levels

Implementations

Armed with the insights gained from conversation analysis, the Credit Union developed a business transformation implementation plan to address the identified opportunities systematically. Cross-functional teams were established to oversee the execution of process improvements, resource reallocations, and technology upgrades. The Credit Union also has access to real-time, continuous feedback loops through their Call Journey CI dashboards and continue to pilot the dissatisfaction executive summary and recommendations module.

Conclusions

The Credit Union’s decision to leverage conversation analysis proved to be a game-changer, uncovering hidden opportunities for cost savings, service improvements and operational efficiency. The $7.5 million in potential savings – just over $4.6m of that in tangible and directly measurable cost/business benefits and efficiencies, not only demonstrated the tangible benefits of data-driven decision-making but also showcased the Credit Union’s commitment to continuous improvement and member satisfaction. This case study serves as a compelling example of how advanced analytics and conversation intelligence can drive transformative change within the Credit Union sector.

Once we had implemented the Call Journey Ci platform, which was super easy, we were staggered with the new and unique insights we could uncover. Additionally, the data and intelligence were far more detailed and context-aware. It showed us how flawed the data we were previously viewing was. We could quickly tie tangible business benefits to those insights – of the roughly $7m of business benefit we could identify, over $4.5m of that benefit we could confidently tie to tangible and directly measurable and correlatable cost and business benefits. And we’re barely scratching the surface

Chief Member Experience Officer